Last year was a special year for large-scale retail trade, both in Italy and all over of the world. Due to the Covid-19 pandemic, in fact, sales have soared in an anomalous way. According to the Observatory of the Italian bank Mediobanca – which aggregated the economic and financial data of 117 Italian companies and 27 major international players for the period 2015-2019 – in Italy 2020 will close with sales growth of +5% for the large-scale retail trade, of which 1% is attributable to the boom in e-commerce. Very marked increases for Discounts (+8.7%), Supermarkets (+6.8%) and Drugstores (+6.6%). The whole system should fall back by 1.6% in 2021, accumulating in the two-year period an increase of 3.3%. E-commerce (+60% in 2021) could reach 3% of the market as early as 2021, two years ahead of the 2023 pre-pandemic forecast.

Click here to discover the authentic Italian F&B products on Italianfood.net platform

In 2020, the concentration on the Italian market is increasing: the market share of the top five retailers is 57.5% (it was 52.8% in 2019). Italy’s retail market concentration surpasses Spain’s (50%), but it is still fragmented compared to France’s (78.1%), Great Britain’s (75.3%) and Germany’s (75.2%).

Data from the large international retailers show a growth in sales by +8.3%, with very positive effects on industrial margins (+17.1%) and net profit (+42.4%).

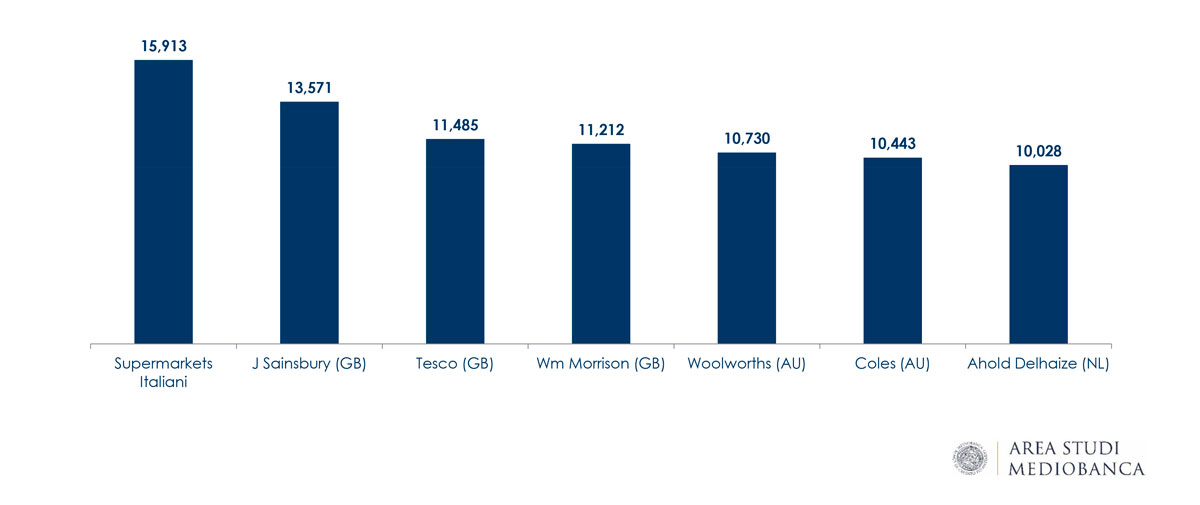

Retail international champions: Sales per square meter of floor space in 2019 (in €)

THE TOP INTERNATIONAL OPERATORS

In 2019, the largest international retailers reported sales ranging from WalMart’s 463 billion euros to Portuguese Jeronimo Martins’ 18.6 billion. These players invoice about 20% of their turnover in stores abroad. The largest international projection is by Dutch Ahold Delhaize (77.6%), followed by Jeronimo Martins (73.3%), French Auchan (62%), and Carrefour (52%).

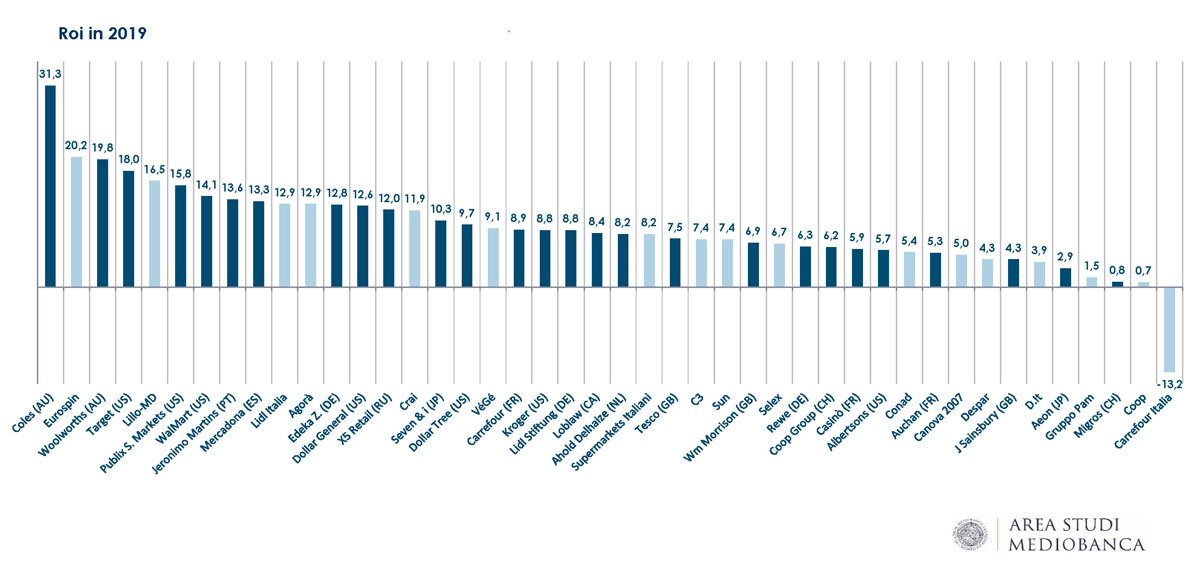

The average Return on Investment (Roi) was 9%. The ranking by Roi sees the Australian Coles (31.3%) in top position, followed by Italy’s Eurospin (20.2%), Australian Woolworths (19.8%), USA Target (18%), and Italian Lillo-MD (16.5%). The performance of the two Iberian companies, Jeronimo Martins (13.6%) and Mercadona (13.3%), was also good.

Supermarkets Italiani is the international leader in terms of sales per square meter within Italy: with 15,900 euros it is ahead of the British companies J Sainsbury (13,600 euros), Tesco (11,500), and Wm Morrison (11,200), as well as the two Australian companies Woolworths (10,700), and Coles (10,400).