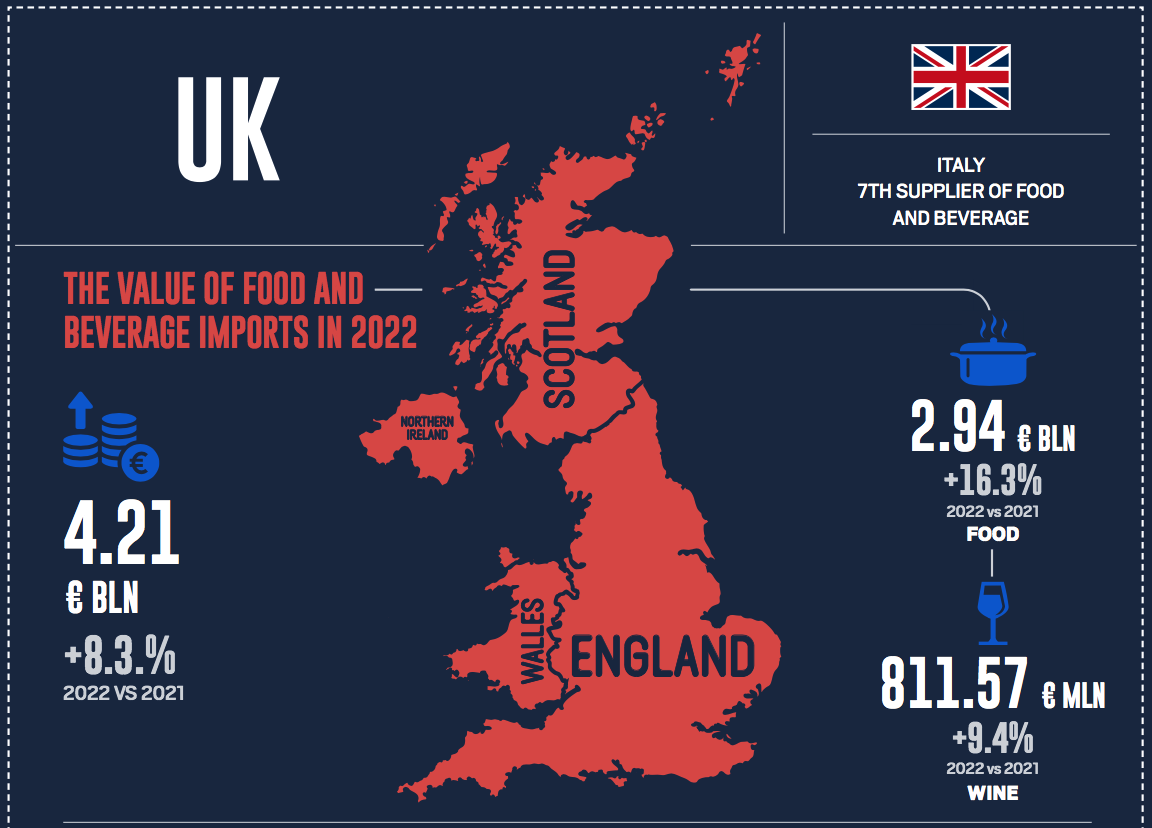

UK imports about 46% of the total food that it consumes: geography, climate, and consumer purchasing power place the country among the most significant importers of food & wine and particularly fresh produce. The food industry continues to face labor shortages, especially of seasonal workers: this is a structural criticality in the country, which currently can only cope with 25% of the required personnel.

THE AIX LONDON-ROME AFTER BREXIT

As a result, supply difficulties are increasing, which will lead to greater dependence on imports in the future. As for Italian food & beverage, in 2022 exports hit a new record of £3.6 billion up 8.3% from 2021.

The analysis of the different production sectors gives us a sharp overview: Italy is the UK’s leading supplier of cheese, pasta and canned tomatoes, the second of wine and oil, close behind France and Spain, and the fifth of fruits and vegetables.

ITALIAN PRIMACY IN ORGANIC…

In the post-Brexit era, purchases of Italian food products have not decreased; but rather there is an increase of the Italian market share from 5.6% to 6.3%. The sectors with the greatest growth potential, especially in the large-scale retail sector, and which Italian companies could exploit the most, is organic: between 2016 and 2021, it has grown in value sales by 30%, reaching £3 billion.

…AND DELIVERY

E-commerce is another channel that is constantly evolving: online food deliveries have increased at an annual rate of 29.4%; the trend is growing and is tied, partly, to the end of the pandemic. In fact, consumers running out of time are increasingly turning to delivery platforms, so much so that between 2022 and 2023 revenues are expected to increase by 7.2% to reach £3.3 billion.

Among the top consumer trends highlighted in this channel is the primacy of Italian cuisine, which according to the 2022 survey conducted by JustEat was the favorite of British consumers with pasta, cheese and lasagna leading the list of most-loved dishes. Speaking again of emerging trends, products from sustainable supply chains will have the greatest likelihood of growth especially in the retail channel. We should not forget that the target consumer of made-in-Italy food is millennial, well-educated and high-income, resi- ding in large cities and, above all, concerned about sustainability.